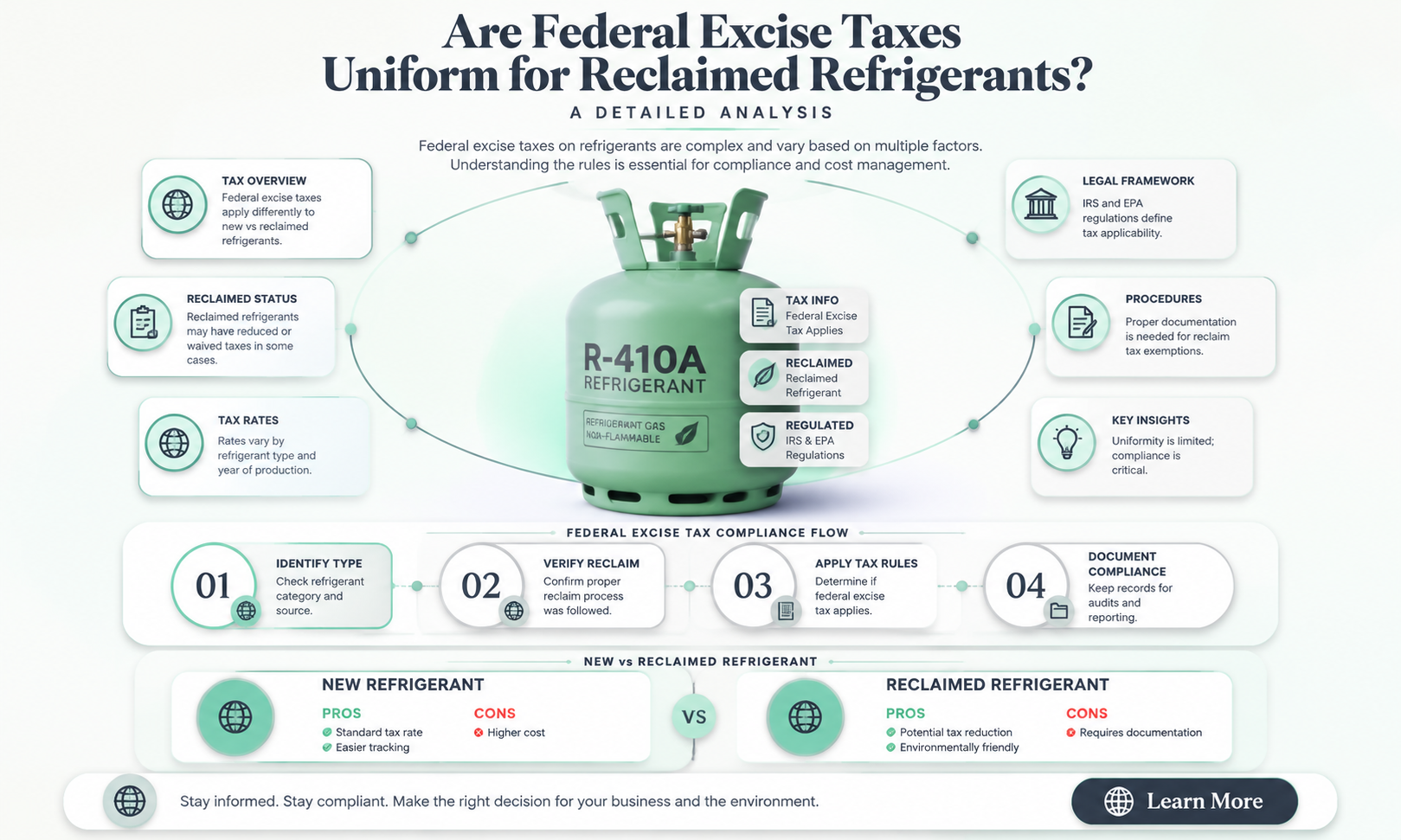

Federal excise taxes on reclaimed refrigerants are a subject of interest for businesses and individuals involved in the HVAC and refrigeration industries. Reclaimed refrigerants, which are recovered, recycled, and restored to meet specific purity standards, play a crucial role in reducing environmental impact and promoting sustainability. However, the question of whether federal excise taxes apply uniformly to these reclaimed substances remains a point of clarification. While the Internal Revenue Service (IRS) imposes excise taxes on certain virgin refrigerants, the treatment of reclaimed refrigerants under these regulations is less straightforward. Understanding the tax implications is essential for compliance and financial planning, as exemptions or reduced rates may apply depending on the specific circumstances and regulatory interpretations.

| Characteristics | Values |

|---|---|

| Tax Applicability | Federal excise taxes generally apply to the sale of virgin refrigerants, not reclaimed refrigerants. |

| Reclaimed Refrigerants Definition | Refrigerants that have been recovered, recycled, and certified to meet virgin refrigerant specifications. |

| Tax Rate for Virgin Refrigerants | $0.20 per pound (as of latest data, subject to change). |

| Tax Rate for Reclaimed Refrigerants | Typically exempt from federal excise taxes, as they are considered recycled products. |

| IRS Guidance | IRS regulations (26 U.S.C. § 4681) specifically target virgin refrigerants, excluding reclaimed ones. |

| Environmental Impact | Reclaimed refrigerants are encouraged for environmental reasons, hence the tax exemption. |

| State Variations | Some states may impose additional taxes or fees on reclaimed refrigerants, but federal excise taxes do not apply. |

| Certification Requirement | Reclaimed refrigerants must meet ARI-700 standards to qualify for tax exemption. |

| Industry Practice | Reclaimed refrigerants are often sold at a lower cost than virgin refrigerants, reflecting their tax-exempt status. |

| Legislative Intent | Federal excise taxes aim to reduce the use of virgin refrigerants, promoting recycling and reclamation. |

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71OcM906MLL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![TurboTax Premier Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71ofxs16-9L._AC_UL320_.jpg)

![TurboTax Home & Business Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71-jbdrZxVL._AC_UL320_.jpg)

What You'll Learn

![]()

Federal Excise Tax Rates on Reclaimed Refrigerants

Federal excise taxes on reclaimed refrigerants are not uniform, and understanding the nuances is crucial for businesses and individuals in the HVAC and refrigeration industries. The Internal Revenue Service (IRS) imposes these taxes under the guise of environmental protection, but the rates and application vary significantly depending on the type of refrigerant and its intended use. For instance, virgin refrigerants typically face a higher excise tax compared to their reclaimed counterparts, which are often taxed at a reduced rate to encourage recycling and reuse. This disparity highlights the government’s effort to balance fiscal responsibility with environmental stewardship.

Analyzing the tax structure reveals a tiered approach. Reclaimed refrigerants, which have been reprocessed to meet industry purity standards, are generally taxed at a lower rate than newly manufactured ones. For example, while virgin HCFC-22 might be subject to a tax of $1.90 per pound, reclaimed HCFC-22 could be taxed at a rate of $0.30 per pound. This significant difference incentivizes the reclamation process, reducing the environmental impact of refrigerant disposal and production. However, the exact rates can fluctuate based on legislative updates and EPA regulations, making it essential for stakeholders to stay informed.

From a practical standpoint, businesses must navigate these tax rates carefully to optimize costs. One actionable tip is to maintain detailed records of refrigerant purchases, including whether the product is virgin or reclaimed. This documentation is critical during tax filings to ensure compliance and take advantage of lower rates for reclaimed refrigerants. Additionally, partnering with certified reclamation facilities can streamline the process, as they often provide documentation that verifies the refrigerant’s reclaimed status, simplifying tax reporting.

Comparatively, the excise tax on reclaimed refrigerants also differs from other environmental taxes, such as those on ozone-depleting substances (ODS). While ODS taxes are often flat rates based on ozone depletion potential, reclaimed refrigerant taxes are more dynamic, reflecting the product’s lifecycle stage. This distinction underscores the importance of understanding the specific tax code sections applicable to reclaimed refrigerants, such as those outlined in the Internal Revenue Code Section 4681. By doing so, businesses can avoid overpayment and allocate savings toward sustainable practices.

In conclusion, federal excise tax rates on reclaimed refrigerants are designed to promote environmental responsibility while providing economic relief to those who participate in recycling efforts. The tiered tax structure, lower rates for reclaimed products, and the need for meticulous record-keeping are key elements businesses must grasp. Staying abreast of regulatory changes and leveraging partnerships with certified reclamation facilities can further enhance compliance and cost efficiency. This nuanced approach not only benefits individual businesses but also contributes to broader environmental goals.

Understanding Heat Pump Refrigerant Capacity: How Much Does It Hold?

You may want to see also

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71pX8Fh2sNL._AC_UL320_.jpg)

![TurboTax Business Desktop Edition 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71iKclcd6ML._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)

![]()

Differences Between Virgin and Reclaimed Refrigerant Taxation

Federal excise taxes on refrigerants are not uniform across all types, and the distinction between virgin and reclaimed refrigerants is a critical factor in understanding their taxation. Virgin refrigerants, which are newly manufactured and have not been used before, are subject to a federal excise tax of $2.70 per pound under the Internal Revenue Code (IRC) Section 4681. This tax is levied at the point of sale by the manufacturer, producer, or importer, and it is intended to address environmental concerns associated with the production and use of new refrigerants, particularly those containing ozone-depleting substances or potent greenhouse gases.

Reclaimed refrigerants, on the other hand, are not subject to the same federal excise tax. Reclamation involves the process of reprocessing used refrigerants to meet the specifications for new refrigerants, ensuring they can be reused in air conditioning and refrigeration systems. The IRS explicitly exempts reclaimed refrigerants from the excise tax, as they are considered environmentally beneficial due to reduced production demands and lower greenhouse gas emissions. This exemption is outlined in IRS regulations, which state that the tax does not apply to refrigerants that have been reclaimed and certified to meet the standards of the American Society of Heating, Refrigerating, and Air-Conditioning Engineers (ASHRAE).

A key practical consideration for businesses is the documentation required to prove that a refrigerant is reclaimed and thus exempt from taxation. Reclaimed refrigerants must be accompanied by a certification from the reclaimer, verifying that the product meets ASHRAE standards. Without this documentation, the refrigerant may be mistakenly taxed as if it were virgin. For example, a HVAC contractor purchasing reclaimed R-22 refrigerant must retain the reclaimer’s certification to avoid inadvertently paying the $2.70 per pound excise tax during audits or tax filings.

From a policy perspective, the tax disparity between virgin and reclaimed refrigerants serves as an economic incentive to promote the use of reclaimed products. By exempting reclaimed refrigerants from taxation, the government encourages businesses to adopt more sustainable practices, reducing the environmental impact of refrigerant production and disposal. However, this system also places a burden on businesses to ensure compliance with documentation requirements, as errors can result in unexpected tax liabilities or penalties.

In summary, while virgin refrigerants are taxed at $2.70 per pound under federal law, reclaimed refrigerants are exempt from this excise tax. This difference reflects broader environmental goals but requires careful attention to certification and record-keeping. Businesses must stay informed about these distinctions to avoid compliance issues and maximize cost savings through the use of reclaimed refrigerants.

Refrigerating Steamed Oysters in Shell: Safe Reheating Tips

You may want to see also

Explore related products

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UL320_.jpg)

![]()

State vs. Federal Excise Tax Policies

Federal excise taxes on reclaimed refrigerants are a niche yet critical area of environmental and tax policy, often overshadowed by broader discussions on energy and sustainability. While the federal government sets baseline standards, states retain significant autonomy in how they implement and enforce these taxes, creating a patchwork of regulations that can confuse businesses and consumers alike. This divergence between state and federal policies highlights the tension between national uniformity and local adaptability, particularly in industries where environmental impact is a pressing concern.

Consider the example of a refrigerant reclamation company operating across multiple states. At the federal level, the Internal Revenue Service (IRS) imposes a $1.40 per pound excise tax on virgin refrigerants but exempts reclaimed refrigerants to incentivize recycling. However, states like California and New York have introduced their own excise taxes on reclaimed refrigerants, citing the need for additional revenue to fund environmental programs. These state-level taxes can range from $0.50 to $1.00 per pound, depending on the state’s specific regulations. For businesses, this means navigating a complex web of tax liabilities that vary by jurisdiction, increasing compliance costs and administrative burdens.

From an analytical perspective, the rationale behind state-level excise taxes on reclaimed refrigerants often stems from a desire to close perceived gaps in federal policy. States with aggressive environmental goals view these taxes as a tool to discourage the use of refrigerants altogether, regardless of their origin. For instance, California’s tax on reclaimed refrigerants is part of a broader strategy to phase out hydrofluorocarbons (HFCs), which have a high global warming potential. However, this approach raises questions about the effectiveness of taxing recycled materials, as it may inadvertently discourage reclamation efforts and push businesses toward less sustainable alternatives.

For businesses operating in this space, understanding the interplay between state and federal policies is essential. A practical tip is to maintain detailed records of refrigerant transactions, including the type, quantity, and destination state, to ensure accurate tax reporting. Additionally, engaging with state environmental agencies can provide clarity on specific regulations and potential exemptions. For example, some states offer tax credits for companies that exceed federal reclamation standards, providing a financial incentive to adopt greener practices.

In conclusion, the divergence between state and federal excise tax policies on reclaimed refrigerants underscores the challenges of balancing environmental goals with economic realities. While federal exemptions aim to promote recycling, state-level taxes reflect localized priorities and funding needs. Businesses must stay informed and proactive to navigate this complex landscape, ensuring compliance while leveraging opportunities to contribute to sustainability efforts. This dual-level regulatory environment serves as a microcosm of broader debates in environmental policy, where uniformity and flexibility often collide.

Refrigerating Tortilla Española: Tips for Storing and Reheating Safely

You may want to see also

Explore related products

$23.99

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

Exemptions for Reclaimed Refrigerants in Excise Taxes

Reclaimed refrigerants, unlike their virgin counterparts, often qualify for exemptions from federal excise taxes. This is because the Internal Revenue Service (IRS) recognizes the environmental benefits of reusing these substances, which reduces the demand for new production and minimizes the release of harmful chemicals into the atmosphere. For instance, under the Internal Revenue Code Section 4682, certain ozone-depleting chemicals (ODCs) are subject to excise taxes, but reclaimed refrigerants are explicitly excluded from this category. This exemption is a strategic move to incentivize businesses and individuals to adopt more sustainable practices in the HVAC and refrigeration industries.

To take advantage of this exemption, it’s crucial to understand the documentation required. Reclaimed refrigerants must meet specific purity standards, typically outlined in industry guidelines like those from the Air-Conditioning, Heating, and Refrigeration Institute (AHRI). A certified reclamation facility will provide a detailed report confirming the refrigerant’s purity and compliance with EPA regulations (40 CFR Part 82). This report is essential when filing tax returns to substantiate the exemption claim. Without proper documentation, businesses risk facing audits or penalties, even if the refrigerant was legitimately reclaimed.

From a practical standpoint, businesses should integrate reclamation into their maintenance schedules to maximize tax savings. For example, during routine HVAC system servicing, technicians can recover used refrigerants, which are then sent to a certified facility for purification. This not only ensures compliance with environmental regulations but also reduces operational costs by avoiding excise taxes. Small to medium-sized businesses, in particular, can benefit significantly, as the savings can offset the initial investment in reclamation services. Additionally, tracking reclaimed refrigerant usage through inventory management systems can streamline the tax reporting process.

A comparative analysis reveals that while exemptions exist at the federal level, state regulations may vary. Some states impose additional taxes or fees on refrigerants, regardless of their reclaimed status. For instance, California’s Refrigerant Management Program includes reporting requirements but does not exempt reclaimed refrigerants from state-level fees. Businesses operating across multiple states must therefore conduct a jurisdiction-by-jurisdiction review to ensure full compliance. This layered approach underscores the importance of staying informed about both federal and state-specific regulations.

In conclusion, exemptions for reclaimed refrigerants in excise taxes offer a win-win scenario for businesses and the environment. By understanding the regulatory framework, maintaining proper documentation, and adopting proactive reclamation practices, companies can reduce their tax burden while contributing to sustainability goals. However, vigilance in navigating federal and state regulations is essential to avoid pitfalls. As the push for greener practices continues, leveraging these exemptions will become increasingly vital for staying competitive in the HVAC and refrigeration sectors.

Easy Steps to Repair Your Stainless Steel Refrigerator Door

You may want to see also

Explore related products

![TurboTax Deluxe Online Edition 2025, Federal Tax Return [Activation Code]](https://m.media-amazon.com/images/I/61bFazlntVL._AC_UL320_.jpg)

![The Taxes, Accounting, Bookkeeping Bible: [3 in 1] The Most Complete and Updated Guide for the Small Business Owner with Tips and Loopholes to Save Money and Avoid IRS Penalties](https://m.media-amazon.com/images/I/617DYgupSxL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![]()

Impact of EPA Regulations on Excise Taxation

The Environmental Protection Agency's (EPA) regulations on refrigerants have a direct and significant impact on excise taxation, particularly in the context of reclaimed refrigerants. As the EPA tightens restrictions on the production and use of virgin refrigerants, the demand for reclaimed refrigerants increases, which in turn affects the excise tax landscape. For instance, the EPA's Significant New Alternatives Policy (SNAP) program has been instrumental in phasing out high-global warming potential (GWP) refrigerants, such as R-22, and promoting the use of more environmentally friendly alternatives, including reclaimed refrigerants.

From an analytical perspective, the EPA's regulations create a ripple effect throughout the refrigerant supply chain. As virgin refrigerant production decreases, the cost of these substances rises, making reclaimed refrigerants a more attractive option for businesses and consumers. This shift in demand has implications for excise taxation, as the Internal Revenue Service (IRS) must adapt its tax policies to reflect the changing market dynamics. For example, the IRS may need to reconsider the tax rates applied to reclaimed refrigerants, taking into account their reduced environmental impact and increased market share. A 2018 study by the American Council for an Energy-Efficient Economy (ACEEE) found that reclaimed refrigerants can reduce greenhouse gas emissions by up to 90% compared to virgin refrigerants, highlighting the need for tax policies that incentivize their use.

To navigate the complexities of excise taxation on reclaimed refrigerants, businesses should follow a series of steps. First, stay informed about EPA regulations and their impact on the refrigerant market. This includes monitoring updates to the SNAP program and other relevant policies. Second, establish a robust system for tracking and documenting the reclamation process, ensuring compliance with EPA standards. Third, consult with tax professionals to understand the specific excise tax requirements for reclaimed refrigerants, which may vary depending on the type of refrigerant and its intended use. For instance, the IRS may apply different tax rates to reclaimed refrigerants used in commercial versus residential settings.

A comparative analysis of excise tax policies across different industries reveals that the treatment of reclaimed refrigerants is not unique. In the fuel industry, for example, the IRS applies a reduced excise tax rate to biodiesel, recognizing its environmental benefits compared to traditional diesel fuel. Similarly, the EPA's regulations on refrigerants could be used to justify a more favorable excise tax treatment for reclaimed refrigerants. However, caution must be exercised to avoid creating unintended consequences, such as a black market for untaxed or improperly reclaimed refrigerants. To mitigate this risk, the IRS should implement strict reporting requirements and penalties for non-compliance, ensuring that the excise tax system supports the EPA's environmental goals without compromising market integrity.

In conclusion, the impact of EPA regulations on excise taxation is a critical consideration for businesses operating in the refrigerant industry. By understanding the interplay between environmental policies and tax laws, companies can make informed decisions about their refrigerant use and reclamation practices. As the EPA continues to promote sustainable alternatives, it is likely that excise tax policies will evolve to reflect the changing market dynamics. For instance, the IRS could introduce tax credits or exemptions for businesses that demonstrate a commitment to using reclaimed refrigerants, further incentivizing environmentally responsible practices. Ultimately, a nuanced approach to excise taxation is necessary to support the transition to a more sustainable refrigerant industry, balancing environmental goals with economic realities.

Understanding the Color of 134a Refrigerant: A Comprehensive Guide

You may want to see also

Frequently asked questions

No, federal excise taxes on reclaimed refrigerants are generally lower or exempt compared to those on virgin refrigerants, as reclaimed refrigerants are considered environmentally beneficial and are often incentivized.

Federal excise taxes on reclaimed refrigerants may vary depending on the specific type of refrigerant and its intended use, but they are typically reduced or waived to encourage recycling and reuse.

Consult the Internal Revenue Service (IRS) guidelines or a tax professional to verify the current federal excise tax regulations for reclaimed refrigerants, as rules may differ based on the refrigerant type and transaction details.

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)